XOLARIS Group2023-03-08T10:05:46+00:00

Swiss Funds vs. Liechtenstein Funds practical view for Investors and Asset managers

Volume of the Swiss market Industry represent somewhere 1.5 billion CHF with almost 10’000 managed funds, while only 1/5 of them, less than 2000 are domiciled in Switzerland.

Historically, Swiss Funds regulatory framework was long time a self-standing island in European regulation. Switzerland had neve been neither part of the EU nor of the European Economic Area (EEA), contrary to Liechtenstein that joined EEA and implemented EU legal framework for funds industry. Thus, Swiss domestic funds market regulation remained for a long time being authentic and not influenced by the EU funds regulations that elaborated unified standard for funds market industry across Europe in the last decade. The situation changed in the last years, whereby Swiss Legislator adopted two laws Financial Institutions Act (FinIA) and Financial Services Act (FinSA) implementing EU Funds regulation framework into swiss domestic legal system from 2020. The laws become finally effective from 2022 for all Swiss domestic funds market. FinIA basically introduced regulatory standards for funds management companies aligned with EU regulation, especially AIFMD, and FinSA introduced standards for market operations conditions aligned with MIFID, specifically covering distribution/placement process of the financial instruments, agent duties in respect of client classification, client categorization, check of the product suitability, transparency requirements as to the product and renumerations, requirements and exemptions from prospectus or KID documentation and other conditions. Nevertheless, the approaching regulatory framework, Swiss asset managers could have not the option to market Swiss funds in other EU countries within the EU passporting system.

In terms of the fund’s creation process while Switzerland is only consider introducing L-QIF, a simplified AIF product regulation, analog to Luxembourg or Cypriot RAIF, current process in Liechtenstein does not require such a complicated product approval procedure as in other European jurisdictions, which allows to process to placements much faster in comparable to other countries’ funds due to simple notification procedures instead of funds authorization procedures.

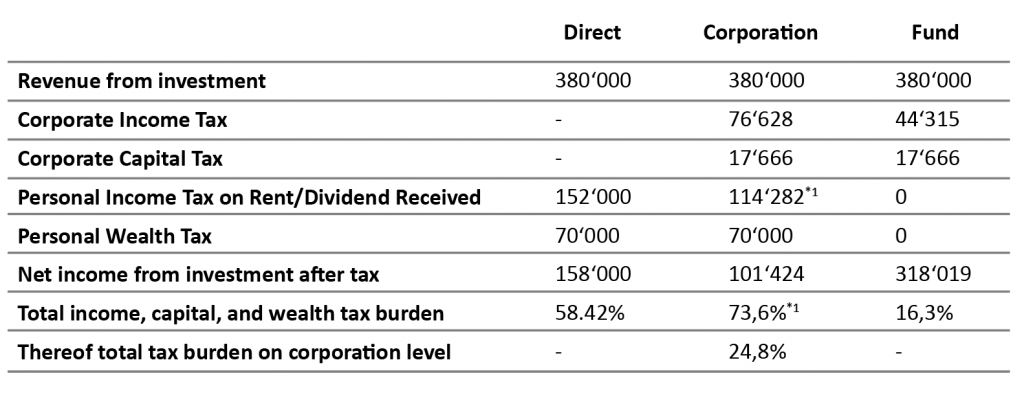

European asset management industry tripled since 2008 and so has real estate class. Funds benefits specifically from tax prospective for real estate investment sector. Direct property ownership in Switzerland through the fund much more tax attractive than corporate or private, effectively making three times less comparing to private holding or almost five time cheaper than corporate holding (combined total income, capital and wealth tax burden, without divined taxed part).

- Simplified distribution with access to other EU placements markets across Europe by simple notification process in the frame of EU passporting system

- Simplified access and contact to the regulating body due to tighten market environment in course of management authorization

- Simplified funds registration procedures (notification vs. authorization)

- Uniform license procedures along with the EU laws allowing managing funds in other EU jurisdictions

- No withholding tax of 35% on distributions to investors comparing to Switzerland

- Constant implementation of the EU regulatory funds updates into national legislation