XOLARIS Group2023-03-08T10:05:04+00:00

Lorem ipsum dolor sit amet, consectetur adipiscing elit. Ut elit tellus, luctus nec ullamcorper mattis, pulvinar dapibus leo.

Germany is ageing. This or something similar has been the headline on the front pages of renowned newspapers and magazines for years. Apart from environmental protection and climate risks, there is hardly any other topic that is regularly discussed, debated and analysed in German talk shows. The spectre of an ageing Germany seems threatening, as it speaks to our innermost fears: the fear of losing control over one's own life at a late age, accompanied by a loss of one's own reputation and the prospect of an uncertain future. From the authors' point of view, however, the much-cited demographic upheaval is no reason for pessimism; on the contrary, it also creates new opportunities and possibilities for the capital investment of institutional investors. The following article will show why an investment in nursing care funds can be a sensible addition to a real estate portfolio.

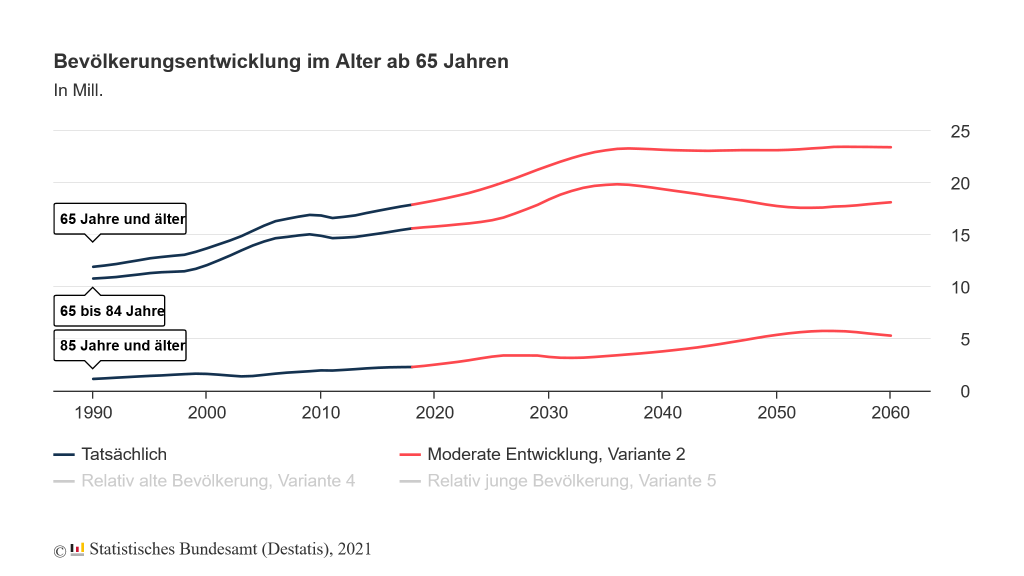

It is undisputed that the proportion of older population groups in Germany will increase significantly over the next 10-20 years. With the demographic development and the constantly changing living environment, the social upheaval is also taking place in the housing market. According to analyses by the Federal Statistical Office (Destatis), the number of people aged 65 and over will increase from the current level of around 15 million by about a third by 2035. The proportion of people aged 85 and over in the total population will continue to increase until 2035 and is not expected to settle at an increased level until 2050.

Fig. 1: Population development at the age of 65 and over

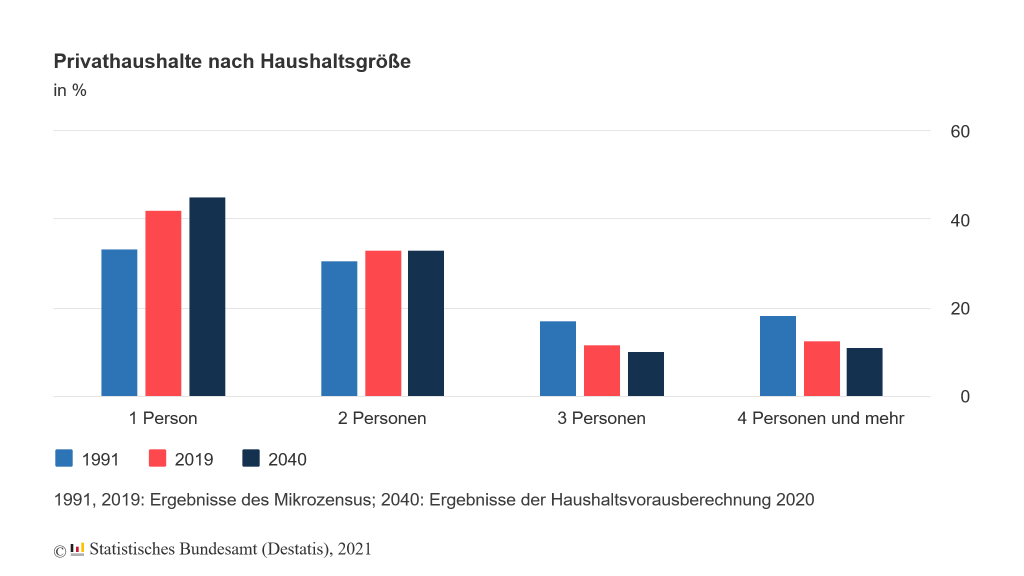

The shift in the age structure is causing professional care services and care facilities to become increasingly important. The trend towards one- or two-person households results in an increasing dependence on third parties. The share of single households is already slightly over 40% and will continue to increase.

Fig. 2: Private households by household size

The trend towards single-person households is certainly also related to the increasing flexibility of younger generations in choosing where to work. Many people in Germany react more flexibly to offers of training, study or work in another federal state The long distances to the home town accordingly make the ongoing care of older family members by younger relatives more difficult.

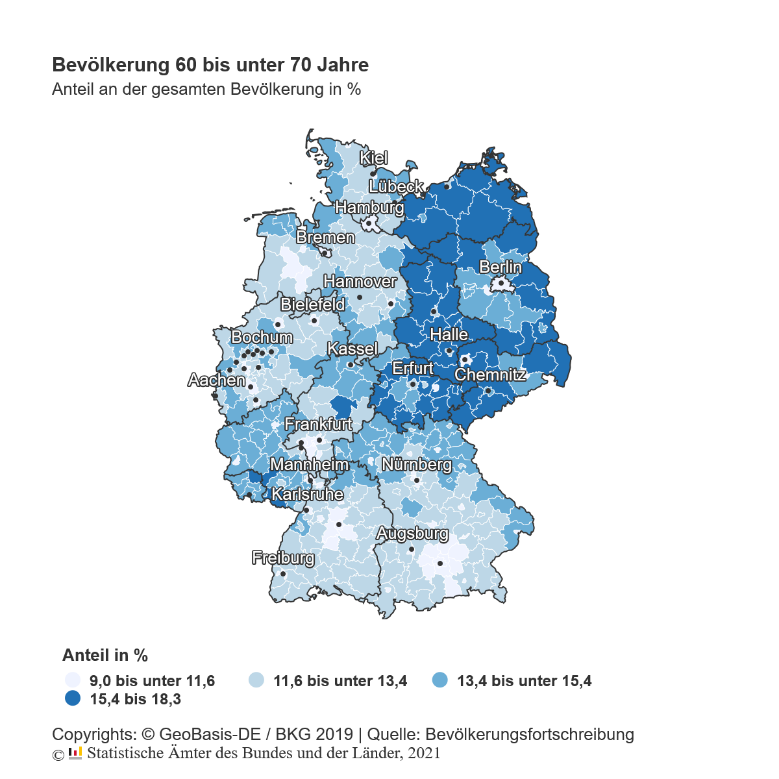

The ageing of the German population is subjectively perceived as inevitable, but requires regional differentiation. The demographic change in the new federal states is much more pronounced than in the old federal states. It is noticeable that the proportion of the population in the age cohorts of 60-70 years or 70-80 years in the new federal states and also structurally weak regions is in some cases twice as high as in the western federal states. Also due to large-scale east-west migration within Germany since reunification, the new federal states are initially most affected by the demographic development.

Fig. 3: Population aged 60 to under 70; source: Destatis, 2021

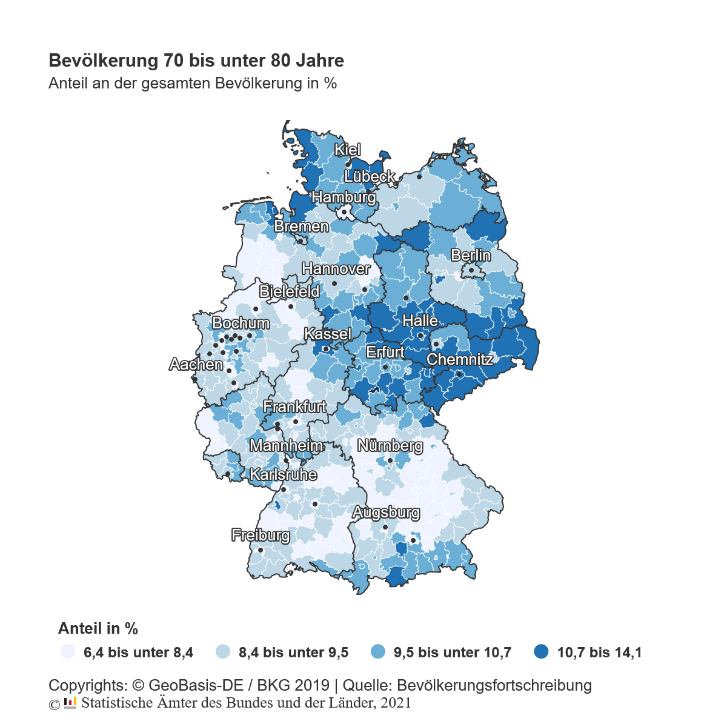

In the coming years, the ageing of society will also become more apparent in the old federal states. Within metropolitan regions such as Berlin, Hamburg or Munich, the population is on average younger than in more remote rural regions due to the constant influx of younger residents. Until now, the quality of life in structurally strong cities and municipalities (until the Corona Pandemic) was decisive as a motivation for moving, also because there have always been more offers of jobs and training places there. These factors together cause a demographic pull effect, which reinforces and accelerates the existing regional age gaps.

Fig. 4: Population 70 to under 80 years old

Germany is ageing, but with regional differences, whereby some regions will continuously rejuvenate, contrary to the general trend.

Most people initially want to live in their own home or at least in their existing environment for as long as possible, even in old age. The option of assisted living initially seems like a sensible alternative to many of those affected. This often fails because the previous own home is not barrier-free or suitable for old age or care. Due to the high mobility of the German population, most relatives are unable to provide care because of their own professional obligations. The change to a nursing home is therefore only postponed as far as possible by assisted living, but is almost unavoidable with higher age.

What is a nursing home?

According to Destatis, 818,300 people were receiving full inpatient care in nursing homes at the end of 2019. In view of the population trends described above, a further decline in the proportion of family members providing care can be assumed in the future. Accordingly, both professional inpatient care in retirement or nursing homes and outpatient care in assisted living concepts will continue to grow in importance.

Both individual residential units in nursing homes and the nursing homes themselves are referred to as nursing properties and are included in the category of social properties. Nursing homes are defined in § 71 of the Eleventh Social Code (SGB XI): They are inpatient facilities in which nursing staff look after people in need of help. Retirement homes, senior citizens’ residences and senior citizens’ residential homes can also be included in this category, provided that these facilities also offer care services.

The special feature from an investor’s point of view is that these are operator properties. The operator market in Germany is largely very small-scale, but increasing consolidation can be observed. Drivers of the dynamic market are investments from Germany and abroad as well as expanding large operator chains. Large operators account for an estimated 40% of the market.

The occupancy rates of nursing homes differ not only regionally, but also according to the operating sponsorship. From a geographical perspective, nursing homes in eastern Germany, in parts of North Rhine-Westphalia or Baden-Württemberg show above-average occupancy rates. The different occupancy rates among the respective operators are mainly the result of reputation reasons or the lack of market penetration of mostly regionally active operators. Supraregional operators can also take advantage of synergy effects, as they are often active in other health care sectors and can build up a bond with future potential care recipients.

Since nursing homes are operator properties, profitability from the owner’s point of view stands and falls with the quality of the operator and the profitability of its concept. Changes in the law can have a massive impact on this.

Strict laws, politicians demand yield caps - risks for nursing home real estate

A study by the IREBS International Real Estate Business School on behalf of the German Property Federation (ZIA) has calculated that up to 293,000 additional nursing home places would have to be created in Germany in the next ten years, which corresponds to between 210 and 390 homes per year, depending on the size of the home and the number of rooms. The authors of the study looked into the question of where the need for nursing homes is greatest. In the inpatient sector, the study comes to the conclusion that most of the people in need of care will have to be cared for in very central locations (virtually in or near the city centre): for example, the study authors assume that the number of people in need of care in Berlin will grow by one third by 2030.

However, the study shows that project developments in peripheral locations away from large cities would be more profitable than in the urban centres, where the need for additional care places will increase. For project developments in central locations to be profitable in the long term, additional incentives and planning security are needed: Land would have to become more affordable or laws would have to allow a larger bed capacity than before. Building requirements such as new energy standards, stricter fire protection regulations or more space consumption due to specifications on the minimum size of rooms also increase construction costs and have a negative impact on costing.

The current regulatory environment leads to a considerable asymmetry between the potential return on a nursing home project in a (very) central location and a nursing home in a peripheral location. However, because the demand for nursing home places is more likely to increase in the conurbations, the asymmetry is intensified: unless there is a relaxation of the legal regulations, additional nursing homes will not be economically viable in the long term where they would have to be built, and where the calculation indicates attractive target returns, there will be a lack of demand in the long term.

Depending on the federal state, there are different specifications for the minimum construction standards. For example, the so-called “single room quota” in Baden-Württemberg and Hamburg is 100%, while other federal states do not have any requirements in this regard. This means that investments always have to be planned and calculated anew depending on the federal state. From the point of view of the study authors, rent indexation would also make sense: Up to now, the nursing homes’ rental contracts have been linked to the consumer price index. The authors of the study are sceptical about the cap on returns for private operators of nursing home facilities demanded by politicians, because this cap as well as the current laws could further reduce the future supply of nursing places.

Care Real Estate in the Corona Pandemic

According to analyses by CBRE and BNP REIM, the German market for healthcare real estate achieved a new record result in 2020 with an investment volume of €3.4-4.0 billion, which was also significantly above the 10-year average. Nursing homes accounted for around 2.7 billion euros of this. International investors were disproportionately represented with a share of 69%, including investors from the Benelux countries with 38% market share and from France with 13%.

As a result of the Corona pandemic, there was high demand for defensive and non-cyclical real estate investments. Rising investor demand, a shortage of products as well as historically extremely reliable cash flows during the pandemic and the economic crisis have caused the prime yield of nursing homes to fall further. German investors in particular have emerged as buyers in recent months, possibly as a special effect of limited travel opportunities for foreign buyers. The dynamics in purchasing behaviour will increase due to the high liquidity in the market. On the other hand, however, product availability is limited.

Outlook: Experts expect prices for care properties to rise

Also in 2021, the investment volume will be limited only by the product supply in view of the high investor demand. More and more German investors appreciate the defensive and non-cyclical asset class of healthcare real estate as a good alternative to other established real estate asset classes. In view of the demographic development in Germany and the high demand for professional care places as well as age-appropriate assisted living facilities, private real estate capital is urgently needed to address the care crisis, which is also reflected in the shortage of care workers.

CBRE expects that the consolidation processes of operators will continue and that larger, economically more sustainable and, from an investor’s point of view, more transparent operator structures will emerge. Foreign investors will also continue to observe the German market for their expansion strategy. With increasing professionalisation and greater transparency of the operator market, the confidence of institutional investors in this alternative asset class is also growing.

Due to the excess demand, the yields for investment-ready products will continue to decline. Currently, the prime yield for nursing homes is still around 4%. After the market was dominated by foreign investors in previous years, domestic investors with strong equity capital are increasingly turning to this asset class. A recent survey by CBRE among German institutional investors revealed that one in four would like to invest in this segment in 2021.

Conclusion

Care properties have proven to be a robust asset class within the special property asset class during the Corona pandemic. The consolidation and professionalisation of operating companies will provide more transparency for institutional investors, also because the German care market is becoming more interesting for foreign players. Due to the long-lasting demographic change in Germany, there are currently still good opportunities to exploit the attractive yield potential of nursing care properties. Regulatory risks exist that could inhibit new project developments or make them unprofitable, and the excess demand for investable nursing care properties is also causing yields to fall. Compared to other real estate investments, nursing care real estate is a sensible addition to a diversified real estate portfolio that covers the entire life cycle of a population through investments in kindergartens, residential and nursing care real estate, in addition to its reliable income and its sustainable social component.